Introduction

The recent Scottish Budget presented by Finance Secretary John Swinney has introduced significant changes to income tax rates, impacting both individuals and businesses across Scotland. These adjustments come at a time when the country is grappling with economic challenges, including rising inflation and the financial needs of public services. Understanding these changes is crucial for residents, employers, and taxpayers to navigate the fiscal landscape effectively.

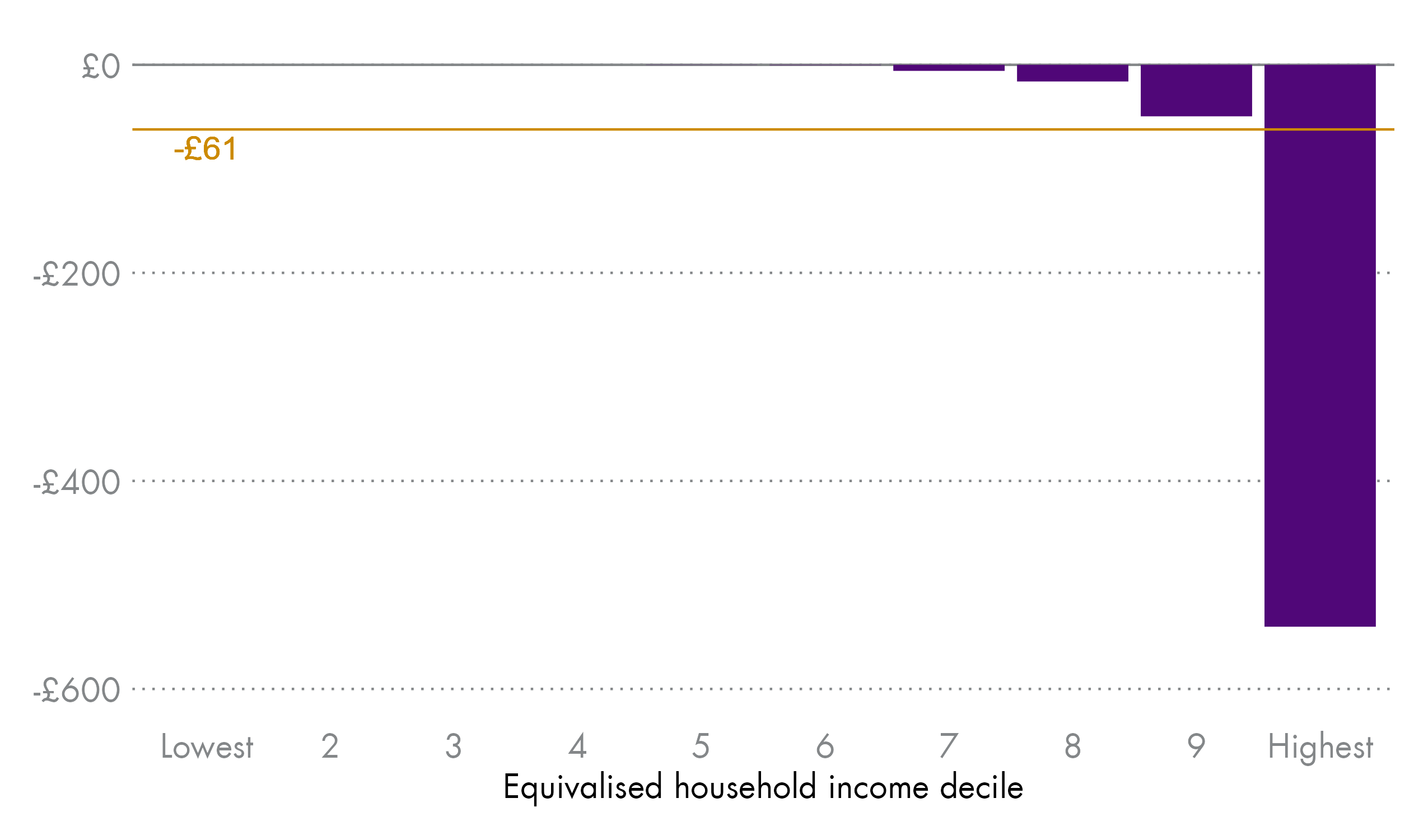

Overview of Income Tax Changes

In the 2023 Budget, the Scottish Government outlined a framework aimed at balancing economic growth with the need for increased public funding. Key changes to the income tax bands have been introduced:

- The higher rate threshold has been adjusted from £43,662 to £45,000, meaning individuals earning above this level will now pay 41% on earnings over this amount.

- The top rate of 46%, applicable for earnings over £150,000, remains unchanged but has been heavily scrutinised due to its potential impact on high earners and investment decisions.

- There are no changes to the basic rate of 20% for earnings between £12,571 and £50,270.

Implications for Taxpayers

These changes will affect various demographics differently. For most workers, the income tax rates will remain stable, allowing clarity in financial planning. However, for higher earners, the adjustments may encourage some to reassess their financial strategies, particularly regarding investments and employment choices.

Furthermore, with the Scottish Budget focusing on increasing revenue to support public services, there is an anticipated rise in funding for areas such as healthcare, education, and social care. The need for adequate funding has become more pronounced, as the government strives to tackle pressing issues such as the NHS backlog and educational resources.

Future Outlook and Significance

The implications of these tax changes will resonate throughout Scotland in the coming years. The balance struck between economic growth and public service funding will be closely monitored by both public and private sectors.

Experts predict that the adjustments could have a mixed impact on Scotland’s economy. While providing necessary revenue for essential services, it may also deter some high earners from remaining in the region. Additionally, ongoing discussions about further economic reforms are expected as the government continues to address fiscal policies to adapt to changing socio-economic conditions.

In conclusion, the Scottish budget income tax changes present both opportunities and challenges, necessitating careful consideration from all stakeholders involved. Keeping abreast of these changes will be vital for financial planning and community development in Scotland.