Introduction

The Bank of England base rate is a critical monetary policy tool that influences the UK economy, affecting borrowing costs, savings rates, and inflation. As economic conditions fluctuate, the Bank of England periodically reviews and adjusts this rate to maintain economic stability and control inflation. Recent developments in the base rate have significant implications for consumers, businesses, and the broader economy.

Recent Changes to the Base Rate

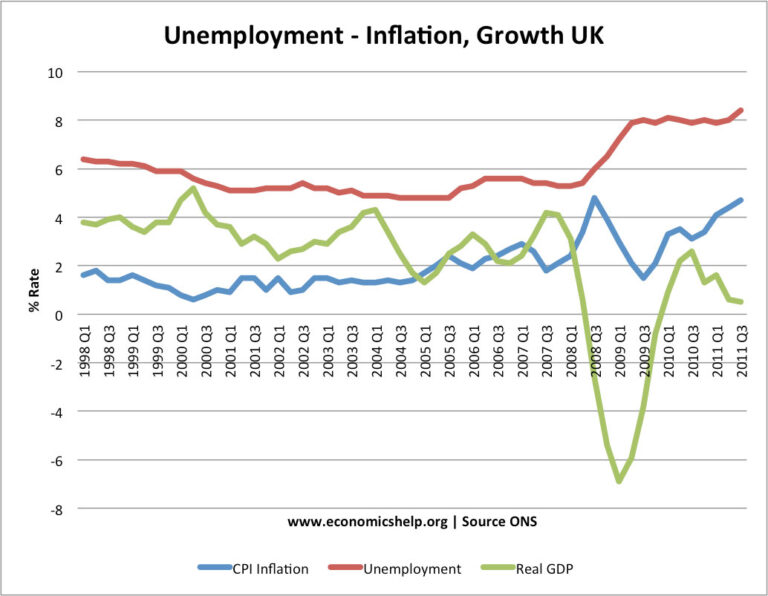

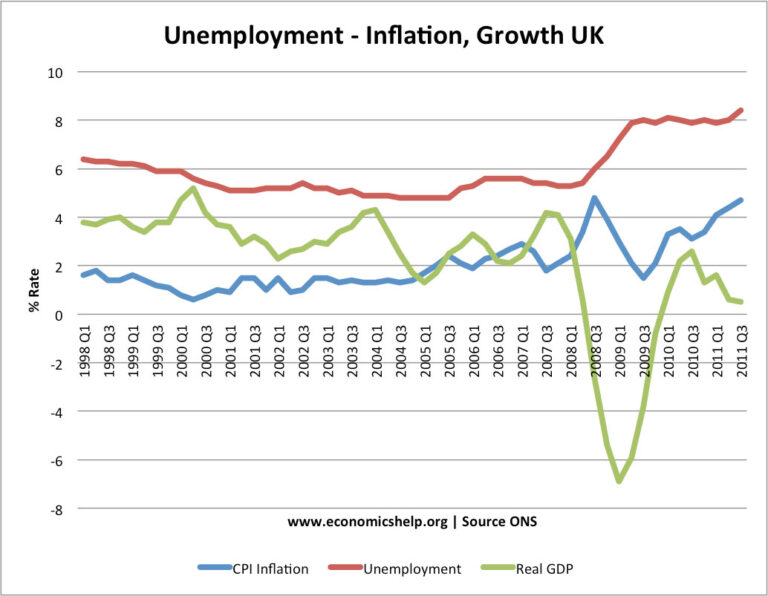

In response to rising inflation and changing economic conditions, the Bank of England announced an increase in the base rate to 5.25% in August 2023, the highest level in over a decade. This decision, made during the Monetary Policy Committee (MPC) meeting, aimed to combat persistent inflation, which has exceeded the Bank’s target of 2%. The increase marks the thirteenth consecutive rise, underlining the serious economic challenges facing the UK.

The Bank of England’s latest inflation report highlighted that while inflation had begun to slow, it remained above 6%, driven primarily by higher energy and food prices. Governor Andrew Bailey noted the need for further tightening of monetary policy to ensure inflation returns to target within a reasonable timeframe. Analysts predict that additional rate hikes may be necessary in the coming months to address ongoing inflation pressures.

Impact on Consumers and Businesses

The rise in the base rate has a direct impact on borrowing costs for consumers and businesses. Mortgage rates, in particular, have surged as lenders pass on the increased costs to borrowers. Nationwide Building Society reported that the average fixed-rate mortgage had reached 6.2% in September 2023, leading many homeowners to reconsider their financial strategies. Additionally, businesses reliant on loans for expansion face higher interest payments, which may constrain growth and investment.

On the other hand, savers are starting to benefit from improved interest rates on savings accounts, prompting some consumers to reconsider their savings strategies. Banks and financial institutions are expected to adjust their rates accordingly, offering more competitive returns to attract deposits.

Conclusion

The Bank of England base rate remains an essential tool for managing the UK economy. As inflationary pressures persist, businesses and consumers alike must navigate the evolving financial landscape shaped by rate adjustments. The significance of the base rate goes beyond immediate financial implications; it reflects broader economic health and central bank strategies. Moving forward, monitoring the Bank of England’s policy decisions will be critical for economic forecasting and personal financial planning.